Saturday, May 17, 2014

Why Israel's Boom Is Actually A Bubble Destined To Pop (English, Russian)

The order of the text was changed. The emphasizing is mine.

There is more below.

Ниже есть продолжение.

...

How Israel’s Economic Bubble Will Pop

...rising interest rates across the yield curve are the most likely catalyst that will pop Israel’s economic bubble. Ultra-low interest rates are the primary driver of Israel’s bubble, so the eventual ending of this condition will cause it to pop. Global and local interest rates are expected to rise in the coming years... , causing central banks to reduce their monetary stimulus policies that have been the source of the bubble-inflating “hot money” capital flows. For example, the U.S. Federal Reserve is expected to fully taper or end its QE3 program in 2014 and there are growing expectations of a Fed Funds rate hike as early as next year.

The popping of the U.S. stock and tech bubbles are another strong risk factor for Israel in the coming years, though this is likely to coincide with the popping of the overall post-2009 global bubble.

There is more below.

Ниже есть продолжение.

Here is what to expect when Israel’s economic bubble truly pops:http://www.forbes.com/sites/jessecolombo/2014/04/29/why-israels-boom-is-actually-a-bubble-destined-to-pop/

* The property bubble will pop, causing prices to fall

* Banks will experience losses on their mortgage portfolios

* The tech bubble will pop in both Israel and the U.S., causing a wave of startup failures (particularly app and social media startups)

* Technology and banking stock prices are likely to fall the hardest, which will drag the overall stock market lower

* Economic growth will go into reverse

* Unemployment will rise

...

Why Israel Has a Tech Bubble

Housing is not the only sector in Israel that is experiencing a bubble; the country’s tech sector has been riding the wave of what I call “Tech Bubble 2.0,” which is primarily centered around companies and startups that are involved with social media, apps, and, to a lesser extent, cloud computing. While many of the technological trends of the past few years are genuine in their own right, I believe that the bubble lies in the frenzied startup and acquisition activity as well as the valuations of companies that operate in the aforementioned arenas.

The overvalued U.S. stock market is acting as a benchmark that is helping to set the tone for the valuations of tech companies and startups. Profitable publicly-traded social media companies such as Facebook and LinkedIn are currently carrying very high valuations, while many others such as Twitter, Pandora, and Yelp have multi-billion dollar market capitalizations without any earnings whatsoever. Recent acquisitions in the technology startup space have also occurred at jaw-dropping valuations such as Facebook’s $$$19 billion acquisition of mobile messaging company WhatsApp and $$$2 billion acquisition of virtual reality company Oculus.

...

While California’s Silicon Valley is the epicenter of Tech Bubble 2.0, the bubble has recently spread to other tech centers around the world, including Israel. As the world’s second-most important startup center after Silicon Valley, Israel has been given the nickname “The Startup Nation” and its tech corridor is nicknamed “Silicon Wadi,” which means “Silicon Valley” in Arabic and colloquial Hebrew. There are currently over 4,800 startups in Israel, including 15 to 20 companies that are likely to launch IPOs in 2014 in New York, London, or Tel Aviv. Israel had 13 companies IPO in the U.S. in 2013, after only 1 U.S. IPO in 2012. Israel’s increasingly frothy startup scene led to a 52 percent surge in demand for web developers last year.

Foreign companies including Facebook, Google, Apple, Intel, IBM, and Cisco, which have been emboldened by their soaring stock prices, have acquired nearly $$$14 billion worth of Israeli tech companies and startups since 2012. Total foreign acquisitions of Israeli companies increased by over 50 percent in value from $$$5.5 billion in 2012 to $$$8.4 billion in 2013. International tech companies are making the same mistakes in their acquisitions of startups in Israel that they are making in Silicon Valley, namely overpaying for speculative startups with little to no earnings and valuing these startups based on their number of users – a throwback to the practices of the late-1990s Dot-com bubble.

In June 2013, Google acquired Israeli GPS app company Waze for $$$1.3 billion, even though it generated only a nominal amount of revenue from advertising and data licensing. Two months later, IBM acquired financial fraud-prevention software company Trusteer for an estimated $$$1 billion despite its comparatively anemic $$$40 million revenues in 2012. In November 2013, website building company Wix went public on the U.S. Nasdaq stock exchange with a lofty $$$750 million market capitalization against $$$55.5 million in revenue and $$$17.8 million in losses in the first nine months of 2013.

In February 2014, Japanese online retailer Rakuten Inc. acquired Israeli Internet messaging and calling service Viber for $$$900 million, even though the company posted just $$$1.52 million in revenue and a net loss of $$$29.51 million in 2013. Total Israeli tech VC exits via IPOs or M&A deals hit a ten year high in 2013, with the average deal value of $$$146 million more than doubling the $$$67 million average deal value of the past decade. Foreign acquisitions of Israeli tech companies have contributed to the shekel’s appreciation in the past couple of years.

The popping of the Israeli tech bubble is likely to coincide with the popping of the tech and stock market bubbles in the United States. Israel has experienced a tech wreck once before when the collapse of the late-1990s Dot-com bubble (combined with the 2001 Israeli/Palestinian Conflict) helped to push the country’s tech-heavy economy into the worst recession since 1953.

On Stanley Fischer: Don’t Mistake a Bubble For Talent

No proper analysis of Israel’s economic bubble should neglect discussing the role played by Stanley Fischer, the governor of the Bank of Israel from 2005 to 2013. Fischer, a New Keynesian economist, has been widely lauded by the international economics community for his management of Israel’s economy during and after the Global Financial Crisis. In 2009, 2010, 2011 and 2012, Fischer received an “A” rating on Global Finance magazine’s Central Banker Report Card, and in 2010, Bank of Israel was ranked the world’s most efficiently functioning central bank. So highly respected is Stanley Fischer that U.S. President Barack Obama nominated him to be Vice-Chairman of the Federal Reserve in January 2014.

I do not share the same reverence for Stanley Fischer that the mainstream economics community does, however. Rather than credit Fischer for Israel’s strong economic performance through the financial crisis, I view his Keynesian-inspired policies as responsible for creating the country’s artificial bubble-driven boom that is, ironically, very similar to those that caused the global crisis in the first place. Like Alan Greenspan’s 2005 departure from the Fed at the peak of the housing bubble that he created, Stanley Fischer left Bank of Israel in 2013 as a hero...but only because “his” bubble has not yet popped. When evaluating central bankers, never mistake a bubble economy for talent.

...

Why Israel’s Offshore Gas Boom May Be Overhyped

The discoveries of the Tamar and Leviathan natural gas fields in the Mediterranean Sea off the coast of Israel has become a source of optimism in recent years as it promises to reduce the country’s energy costs and allow it to eventually become a net energy exporter. While Israel is undoubtedly fortunate to have discovered this natural bounty, there is reason to believe that its potential economic impact is being overstated by the media, the government, and the business community.

According to a recent Ernst and Young study, the Tamar and Leviathan gas fields are worth $$$52 billion in total capitalization value to Israel’s economy over the next 28 years, with domestic energy cost savings accounting for $$$42 billion of this figure and royalties and taxes on gas suppliers’ profits accounting for $$$10 billion. When spread across 28 years, offshore natural gas resources are expected to provide $$$1.86 billion in annual value to Israel’s economy. A $$$1.86 billion annual windfall is certainly nothing to sneer at, but what is overlooked is the fact that its expected contribution to Israel’s $$$242.9 billion GDP is a “drop in the bucket” of 0.76 percent – hardly the economic game-changer that it is being hyped up to be.

In addition, the estimated value of Israel’s offshore natural gas may be overly optimistic because it assumes that the country will be able to export its excess gas to neighboring countries including Turkey, Jordan, and Egypt within the next several years. Unfortunately, volatile relations between Israel and its potential gas export partners are likely to hamper the cooperation that is required for Israel’s goal of being a net energy exporter to become a reality.

The difficulties of finding reliable export partners for the region’s natural gas are the reason why a recent piece in The Economist magazine claimed that Israel and other Eastern Mediterranean countries may be “fooling their people with false promises of an offshore gas bonanza.” The Economist piece also quotes energy analysts who state that Israel is “unlikely ... to start exporting large amounts by 2020, as it hopes.”

...

...Record low interest rates in the U.S., Europe, and Japan, along with the U.S. Federal Reserve’s multi-trillion dollar quantitative easing programs, caused $$$4 trillion of speculative “hot money” to flow into emerging market investments over the last several years. A global carry trade arose in which investors borrowed cheaply from the U.S. and Japan, invested the funds in high-yielding emerging market assets, and earned the interest rate differential or spread. Soaring demand for emerging market investments led to a bond bubble and ultra-low borrowing costs, which resulted in government-driven infrastructure booms, dangerously rapid credit growth, and property bubbles in countless developing nations across the globe.

Capital inflows into Israel immediately increased after the financial crisis and hit a record high of $$$7.22 billion in the fourth quarter of 2013:

Source: Trading Economics

Strong capital inflows are the reason why Israel has been able to maintain a current account surplus despite the country’s growing trade deficit over the past decade.

Foreign “hot money” inflows into Israel contributed to a 23 percent increase in the shekel currency’s strength against the U.S. dollar since the financial crisis:

To stem Israel’s export-harming currency strength and support economic growth, the country’s benchmark interest rate, prime rate, and effective interbank rate were cut to all-time lows:

Source: Trading Economics

Source: Trading Economics

Source: Trading Economics

The global bond bubble and safe-haven demand helped to push 10 year Israel government bond yields down to a record low of just 3.34 percent after the financial crisis:

Source: Trading Economics

Exports account for approximately 40 percent of Israel’s GDP, which means that the country’s economy is adversely affected by appreciation of the shekel currency. For the past six years, Bank of Israel has been waging a war against the strong shekel – the world’s best performing major currency in 2013 – with a combination of ultra-low interest rates and aggressive currency interventions.

Since 2008, Bank of Israel has purchased over $$$50 billion worth of foreign currencies with newly created or “printed” shekels in an attempt to weaken the currency. As a result, Israel’s M1 money supply, which includes physical cash and demand deposits (typically checking accounts), surged by 150 percent even though the country’s real GDP grew by only 22 percent:

Source: Trading Economics

Unsurprisingly, Israel’s low interest rate, surging money supply environment of the past half-decade has resulted in inflation and asset bubbles. The quadrupling of the Israeli Consumer Price Index between June 2007 and June 2011 led to massive street protests in 2011 and 2012 that drew hundreds of thousands of participants.

Israel’s inflation protests fixated particularly on the rising cost of food, energy, and housing, which is partly due to the housing bubble... While Israel’s inflationary pressure abated somewhat after Bank of Israel hiked interest rates from late-2009 to late-2011, inflation may rear its ugly head again now that interest rates have been reduced to record lows for the second time since the global financial crisis. Israel’s M1 money supply growth stabilized in 2010 and 2011 thanks to rising interest rates and the weakening shekel, but has grown by nearly a third since the start of 2012 after Bank of Israel cut rates and intervened as the shekel began to strengthen again.

Israel Has A Property Bubble

Israel’s record low interest rates and rapid money supply growth after the financial crisis has created a property bubble in which prices have soared by 80 percent since 2007 and 67 percent since 2009:

Since 2006, Israel has experienced the largest property price increase among OECD nations. Israel’s property price increases have far outpaced the country’s average nominal income gains of 23 percent since 2007 and 12.5 percent since 2009, which has contributed to the public’s growing discontent over the rising cost of living. In the year ended Q3 2013, Haifa, Gush Dan, and Tel Aviv saw the largest price increases with respective gains of 25.2 percent, 15.2 percent, and 12.7 percent. Tel Aviv, Sharon, and Jerusalem are Israel’s most expensive housing markets with average prices of owner-occupied dwellings of ILS2,250,900 (US$$$642,870), ILS1,535,900 (US$$$438,662), and ILS1,497,200 (US$$$427,609) in Q3 2013 respectively.

Several affordability and valuation ratios show that Israel’s housing market has become overvalued and far less affordable in the past half-decade as the bubble inflated. From 1996 to 2008, Israel’s average apartment price-to-average monthly salary ratio remained stable at 100, but has surged to 130 in recent years. A recent IMF study showed that Israel’s home prices are now 25 percent above their equilibrium value as measured by price-to-income and price-to-rent ratios that are 26 percent and 22 percent above their long-term levels. Israel’s low average gross rental yield of 3.45 percent is also indicative of an overvalued property market.

Israel’s price-to-rent ratio understates the true extent of the country’s housing bubble because rents themselves have been experiencing what can be considered a type of bubble. Since 2008, the average rent in Israel has risen by 49 percent, with larger increases of 61 percent and 53 percent in Tel Aviv and Sharon. The average rent rose from 30 percent of the average salary in 2007 to 38 percent in 2013, with rent consuming an alarming 56 percent of the average salary in Tel Aviv.

Israel’s Ministry of Construction and Housing (MOCH) claims that the country’s soaring rents are primarily driven by demand for investment properties, which has increased as a result of the ultra-low interest rate environment. A 2013 Bank of Israel study showed that the percentage of households that own at least one home for investment purposes increased by nearly 150 percent from 2003 to 2013. In Tel Aviv, which is Israel’s most inflated housing market, investors account for 29 percent of all home purchases. While foreign investors are often blamed for Israel’s soaring property prices, they account for a small and declining proportion of the country’s overall property sales. Foreign purchases of Israeli homes dropped from 6 percent of all home purchases in 2005-06 to 3 percent in 2009 and 4.1 percent in 2011.

Israel’s property market has inflated on the back of a mortgage bubble that has grown as a result of mortgage interest rates that have dramatically decreased in the past decade:

According to Bank of Israel, total outstanding household mortgage debt increased 78 percent from NIS136 billion at the end of 2007 to NIS242 billion at the end of 2012. Israel’s banks are exposed to the country’s housing bubble because mortgages and loans to real estate businesses account for approximately 40 percent of their assets. Even more worrisome is the fact that approximately 90 percent of new mortgages originated during the peak of the bubble have adjustable interest rates, which is evidence that Israel is making one of the key mistakes that the U.S. made during last decade’s housing bubble. When Israel’s artificially low interest rates eventually rise again, monthly payments on adjustable rate mortgages will rise and put homeowners and banks in jeopardy.

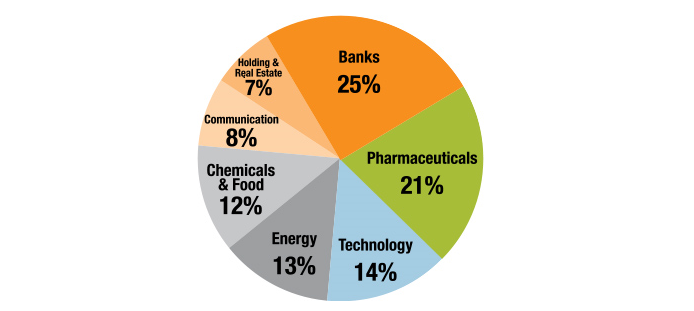

Israel’s entire economy is exposed to the housing and mortgage bubble because banking is one of the country’s key industries. Banking and real estate companies account for a combined one-third of the benchmark Tel Aviv-25 stock index’s capitalization:

Source: Tel-Aviv Stock Exchange

Israel’s growing economic bubble has helped the banking and real estate-heavy Tel Aviv-25 stock index to triple in the past decade:

Source: Trading Economics

Like many nations outside of the hard-hit U.S. and Europe, Israel’s inflating housing bubble helped to boost the country’s consumer spending in the wake of the global financial crisis. Unfortunately, this wealth effect is not sustainable and will actually reverse when Israel’s housing bubble pops.

Сатановский: Пришли ракеты Яхонт - разбомбили ракеты Яхонт

но после того, как они были сданы покупателю

Ещё раз заплатят, ещё раз поставим. То же самое с Бушерской атомной станцией...Главное, чтобы российские специалисты не пострадали...

Ещё раз заплатят, ещё раз поставим. То же самое с Бушерской атомной станцией...Главное, чтобы российские специалисты не пострадали...

Егишянц: Через годик ждём фейерверка на фондовых рынках?

...Аналитики снова отмечают критические уровни по большинству долгосрочных индикаторов рынка – так что вполне вероятны пики зимой-весной и после колебаний в течение 8-10 месяцев обвал (ну плюс-минус полгода к этим срокам), хотя кое-кто ждёт худшего лишь после президентских выборов, т.е. уже в 2016 году (ага, в 2008 году тоже многие так думали). Пока же начинают потихоньку вырисовываться окончательные цели по ведущим индексам США: нам представляется, что Dow Jones идёт в 18000/18500, S&P-500 намылился в 2100/2200; NASDAQ Composite явно очень хочет потрогать пик 2000 года (около 5200) – так что он, видимо, развернётся где-то от зоны 5000/5500 пунктов. От текущих уровней указанные значения отстоят на 10-30% - так что скорее всего на восхождение и впрямь уйдёт ещё полгода-год...http://www.itinvest.ru/analytics/reviews/world-markets/8245/

...любопытным является несоответствие фасада внутреннему содержанию – в целом всё дико растёт, но крупные спекулянты потихоньку урезают рисковые позиции в пользу кэша и облигаций: вообще, из активов они предпочитают консервативные (например, европейские) – побудив физиков пуститься во все тяжкие (разумеется, только тех, у кого вообще есть свободные деньги), институционалы постепенно начинают фиксировать прибыль; обычно так бывает в финальных стадиях раздувания пузырей. И ещё один аргумент – расхождение развитых и развивающихся рынков и экономик: первые пухнут, а вторые стагнируют – часто пузырь служит "пылесосом", высасывающим деньги со всего мира в пользу избранных. Через годик ждём фейерверка?

...сырьё станет дорожать – на что есть неплохие шансы...По-прежнему сильны пшеница, кукуруза, соя, рапс, сахар, кофе, какао, фрукты, хлопок, корма, мясо и молоко – впрочем, на свежие максимумы сподобилась лишь говядина, всё остальное ведёт себя поспокойнее. Однако наш прогноз остаётся в силе – во втором полугодии сырьё и еда должны будут ещё подорожать.

Subscribe to:

Comments (Atom)